-

Manbhawan-5

Lalitpur, Nepal

-

You may send an email

connect@finedusheel.org

-

Helpline and support

015420252

Manbhawan-5

You may send an email

Helpline and support

February 20, 2026

Nepal’s banking system has achieved remarkable growth over the past decade. As of Asoj 2082, total credit outstanding reached NPR 5.67 trillion, serving a population of 29.16 million through A, B, and C class banks and financial institutions (BFIs). Branch networks now exceed 6,500 nationwide, reflecting a significant expansion in physical outreach.

Yet behind this impressive scale lies a structural imbalance: credit remains heavily concentrated geographically, with Kathmandu and Bagmati Province capturing the lion’s share of financial resources. This concentration is not merely a reflection of urban economic activity; it poses systemic risks and threatens the very goals of inclusive financial development.

Consider the following figures:

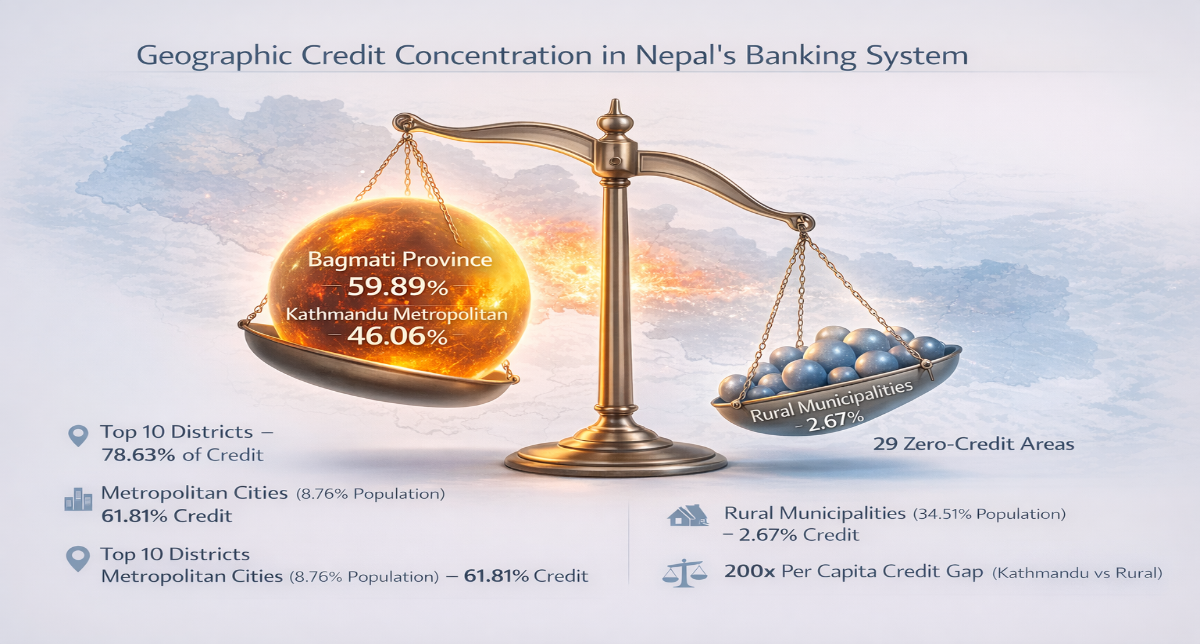

In per capita terms, a resident of Kathmandu has access to over 200 times more credit than a resident in a rural municipality. This is structural financial centralization, not urban strength, and it signals systemic vulnerability.

The provincial credit landscape reveals a sharp imbalance:

Key observations:

Such disparities are not only inequitable but also pose macroprudential risks. If Kathmandu faces an economic shock, the concentrated exposure could ripple across the entire banking system.

Kathmandu Metropolitan City alone demonstrates extreme centralization:

The city holds nearly half of Nepal’s formal credit while accounting for less than 3% of the population, yielding a credit-to-population concentration ratio exceeding 15:1.

Credit access across local body categories highlights structural exclusion:

Critical findings:

Despite 6,526 branches nationwide, provinces with significant networks remain underfinanced. Credit approval and booking continue to be centralized, and corporate headquarters clustering inflates Kathmandu-based exposure. While branch expansion supports deposit mobilization and transaction services, it has not produced equitable credit distribution.

The goal is balanced risk diversification, not forced redistribution.

A geographically diversified credit portfolio strengthens:

Credit concentration is not just a developmental issue—it is macroprudential exposure. Nepal can achieve scale in banking, but without structural balance, inclusive financial development remains unattainable.

Nepal’s banking sector has expanded impressively, but growth without balance is unsustainable. Allocating 61.81% of credit to just 8.76% of the population is a structural imbalance that risks economic stagnation outside the capital.

The solution is clear: risk diversification, opportunity equalization, and financial federalism. Political federalism alone cannot succeed without its financial counterpart.

Nepal stands at an economic crossroads. To graduate from least-developed status, boost domestic production, and reduce reliance on remittances, the entire country must access formal credit—not just Kathmandu. A banking system that finances only its capital neglects the nation.

The data is unmistakable. The imbalance is measurable. The conversation is overdue. Inclusive growth demands that financial decentralization follow political federalism. Otherwise, aggregate credit growth will remain a hollow victory, flowing only to a few while the rest of Nepal is left behind.